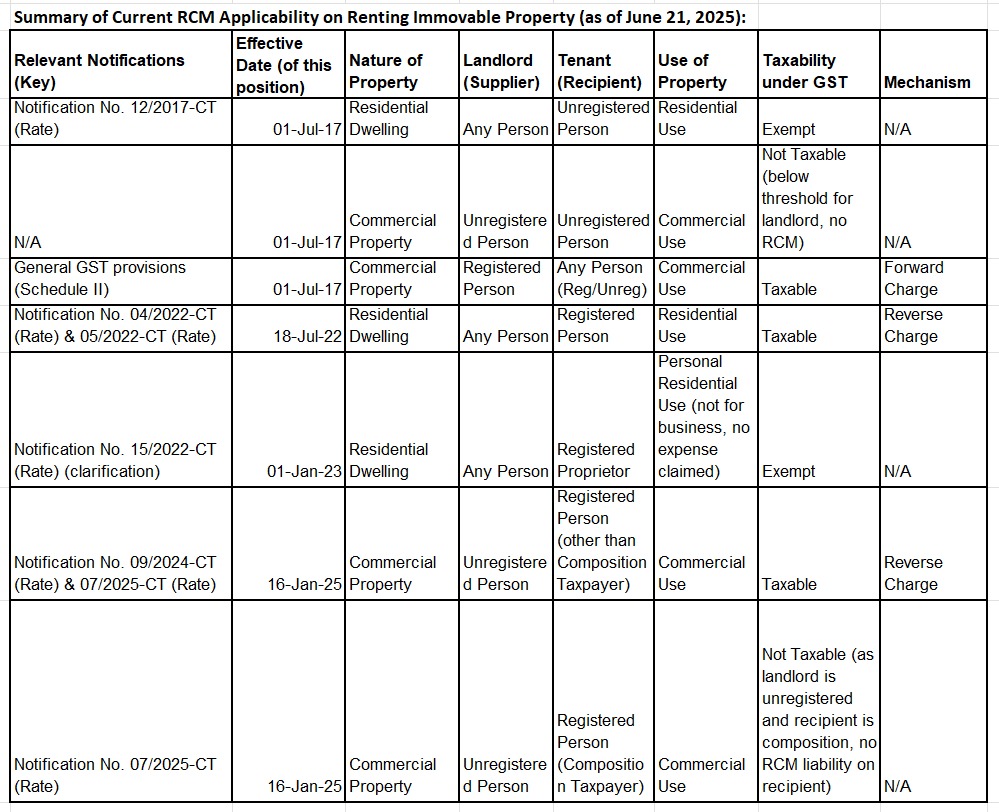

Reverse Charge Mechanism (RCM) under GST on Renting of Immovable Property: A Historical and Current Perspective

The Reverse Charge Mechanism (RCM) under Goods and Services Tax (GST) significantly alters the traditional "forward charge" liability, shifting the responsibility of paying GST from the supplier to the recipient of services. This mechanism has seen notable evolution concerning the renting of immovable property in India, impacting both residential and commercial sectors.

GOODS AND SERVICES TAX (GST)

CA Kamal Kishore

6/21/20253 min read

Early Days of GST (July 1, 2017 - July 17, 2022)

From the inception of GST on July 1, 2017, the general principle was that:

Renting of commercial properties was taxable under the forward charge mechanism (FCM) at 18%, meaning the landlord (supplier) was responsible for collecting and remitting GST. This applied if the landlord was registered under GST and the tenant could be registered or unregistered.

Renting of residential dwellings for residential purposes was unconditionally exempt from GST. This was covered under Notification No. 12/2017-Central Tax (Rate) dated 28th June 2017, specifically at Sl. No. 12. This exemption applied regardless of whether the landlord or tenant was registered or unregistered, as long as the property was used for residential purposes.

During this period, RCM was generally not applicable to the renting of immovable property.

Introduction of RCM on Residential Dwellings (Effective July 18, 2022)

A significant change was introduced following the 47th GST Council Meeting recommendations, bringing the renting of residential dwellings to registered persons under the ambit of RCM.

Notification No. 04/2022-Central Tax (Rate) dated 13th July 2022: This notification amended the existing exemption Notification No. 12/2017-Central Tax (Rate). The exemption for "services by way of renting of residential dwelling for use as a residence" was now qualified with "except where the residential dwelling is rented to a registered person." This meant that if a residential dwelling was rented to a person registered under GST, the exemption was withdrawn.

Notification No. 05/2022-Central Tax (Rate) dated 13th July 2022: To implement the above, this notification amended Notification No. 13/2017-Central Tax (Rate) (which lists services liable to RCM). A new entry (Sl. No. 5AA/6AA, depending on the integrated tax notification) was inserted, making the recipient (registered person) liable to pay GST under RCM for "service by way of renting of residential dwelling to a registered person."

Date of Applicability: Both Notification No. 04/2022-Central Tax (Rate) and Notification No. 05/2022-Central Tax (Rate) came into effect from 18th July 2022.

Impact: From July 18, 2022, if a residential dwelling was rented to a person registered under GST (even if for residential use), GST at 18% became applicable under RCM, with the registered tenant being responsible for paying the tax.

Clarification for Proprietors (Effective January 1, 2023): There was initial confusion regarding registered proprietors renting residential dwellings for their personal use. To address this, Notification No. 15/2022-Central Tax (Rate) dated 30th December 2022 was issued, effective from 1st January 2023. This notification clarified that the RCM would not apply if a residential dwelling is rented to a registered person who is a proprietor and rents the property for their personal use (not for business purposes), and the rental expenses are not claimed as business expenses in their books of accounts.

Recent Development: RCM on Commercial Property (Effective October 10, 2024, with subsequent amendment)

Another significant change impacting commercial property rentals under RCM was introduced recently.

Notification No. 09/2024-Central Tax (Rate) dated 8th October 2024: This notification brought the renting of any commercial or immovable property (other than a residential dwelling) by an unregistered person to a registered person under the RCM.

Date of Applicability: This notification was effective from 10th October 2024.

Subsequent Amendment for Composition Taxpayers (Effective January 16, 2025): Following the 55th GST Council meeting, an amendment was introduced to provide relief to composition taxpayers.

Notification No. 07/2025-Central Tax (Rate) dated 16th January 2025: This notification amended Notification No. 13/2017-Central Tax (Rate) (which governs RCM). Specifically, for the service of "renting of any immovable property other than residential dwelling" (Sl. No. 5AB), the RCM would apply if the supplier is an unregistered person and the recipient is "Any registered person other than a person who has opted to pay tax under composition levy."

Date of Applicability: This amendment came into effect from 16th January 2025.

Impact: As of January 16, 2025, if an unregistered landlord rents out a commercial property to a GST-registered person (other than a composition taxpayer), the registered tenant is liable to pay GST under RCM. If the registered tenant is a composition taxpayer, RCM will not apply, and the transaction effectively remains outside the GST net (as the unregistered landlord is not liable to collect GST).