TDS on interest and remuneration paid to partners by a partnership firm in India

The Finance (No. 2) Act, 2024, introduced Section 194T to mandate TDS on certain payments made by a firm to its partners. This is a significant change aimed at enhancing transparency and ensuring timely tax collection.

INCOME TAXTDS

CA Kamal Kishore

6/23/20253 min read

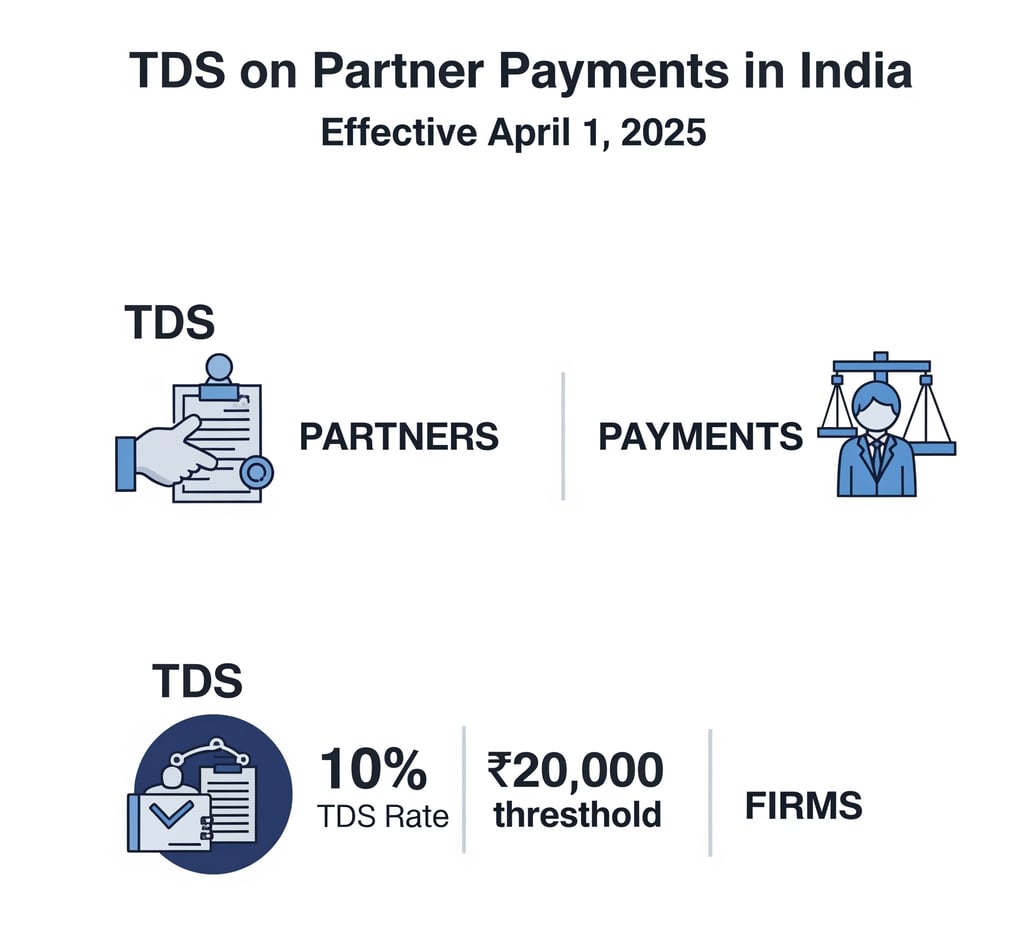

There have been significant changes regarding TDS on interest and remuneration paid to partners by a partnership firm in India, effective from April 1, 2025, with the introduction of Section 194T of the Income Tax Act, 1961.

Here's a brief overview of the provisions:

Before April 1, 2025:

Interest to Partners: Generally, interest paid by a partnership firm to its partners was exempt from TDS under Section 194A. This was because the relationship between a firm and its partners was not considered that of a debtor-creditor in the traditional sense, and such interest was considered an appropriation of profit.

Remuneration (Salary, Bonus, Commission) to Partners: Similarly, remuneration paid to partners was also not subject to TDS under Section 192 (TDS on Salary) as partners are considered owners, not employees, and there's no employer-employee relationship. These payments were taxable in the hands of the partners as business income under "Profits and Gains from Business or Profession" (PGBP).

From April 1, 2025 (Introduction of Section 194T):

The Finance (No. 2) Act, 2024, introduced Section 194T to mandate TDS on certain payments made by a firm to its partners. This is a significant change aimed at enhancing transparency and ensuring timely tax collection.

Key Provisions of Section 194T:

Applicability: This section applies to any person, being a firm, responsible for paying certain sums to a partner of the firm. This includes traditional partnership firms and Limited Liability Partnerships (LLPs).

Payments Covered: The following payments made by a firm to a partner are now subject to TDS under Section 194T:

Salary

Remuneration

Commission

Bonus

Interest on Capital

Interest on Loan

TDS Rate: The rate of TDS is 10%.

Threshold Limit: TDS is to be deducted only if the aggregate of such sums (salary, remuneration, commission, bonus, interest on capital, and interest on loan) credited or paid, or likely to be credited or paid, to a partner during the financial year exceeds ₹20,000.

Important Note: Once the aggregate payments cross this ₹20,000 threshold, TDS applies to the entire amount, not just the portion exceeding the threshold.

Timing of Deduction: TDS must be deducted at the earlier of the following:

At the time of credit of such sum to the account of the partner (including the capital account).

At the time of payment thereof (in cash, cheque, draft, or any other mode).

Payments NOT Covered:

Withdrawals from Capital Account Balance: Repayment of capital contributed by a partner is not considered income and thus, is not subject to TDS under Section 194T.

Reimbursements for Business Expenses: If a firm reimburses genuine business expenses incurred by a partner, it's not subject to TDS.

Share of Profit: A partner's share of profit from the firm is exempt from tax under Section 10(2A) of the Income Tax Act in the hands of the partner, and therefore, no TDS is applicable on it.

No Exemptions/Lower TDS Certificates for Partners: Unlike many other TDS provisions, partners cannot submit Form 15G/15H or apply for a lower/nil TDS certificate under Section 197 for payments covered under Section 194T. The 10% TDS deduction is mandatory if the threshold is crossed.

Compliance Requirements for Firms:

Obtain TAN: Firms must have a Tax Deduction and Collection Account Number (TAN) if they don't already have one.

Deduct and Deposit TDS: Ensure timely deduction and deposit of the TDS with the government.

File TDS Returns: File quarterly TDS returns (Form 26Q or 27Q for non-residents).

Issue TDS Certificates: Provide Form 16A to the partners, enabling them to claim credit for the TDS deducted in their individual income tax returns.

Consequences of Non-Compliance:

Failure to deduct or deposit TDS as per Section 194T can lead to:

Interest: 1% per month for failure to deduct TDS and 1.5% per month for failure to deposit deducted TDS.

Penalties: Penalties for non-compliance, including a late filing fee of ₹200 per day for non-filing of TDS returns (capped at the total TDS amount).

Disallowance of Expenses: 30% of the expense (remuneration/interest) may be disallowed under Section 40(a)(ia) of the Income Tax Act for non-deduction of TDS.

This new section significantly increases the compliance burden on partnership firms and LLPs, requiring them to maintain meticulous records of payments to partners and ensure adherence to the new TDS regime.